Bank Cheques Automation

Bank Cheques Automation

Bank Cheques Automation is an Intelligent Process Automation product that automates the process of clearing cheques. Using a combination of proprietary advanced technologies such as Computer Vision, Computational Geometry & Machine Learning Bank Cheques Automation extracts information from a cheque and validates the information including automated signature verification (ASV). It has a functionality for manual override for agents to edit the information. The cheque must be in English. Other languages are not supported as of now.

How does Bank Cheques Automation work?

Setting up

Bank Cheques Automation integrates with the bank’s workflow using a simple plug-and-play API.

Identification

Its region-of-interest detector identifies each element of the cheque.

Extraction

It processes the segregated checks at near 100% accuracy.

Segregation

Based on scan quality, it segregates the cheques into processable and non-processable streams. The latter is directly sent for human intervention. Currently Bank Cheques Automation supports about 85% of Cheques.

Validation

It then validates the data — date is within 90 days, amount in words and figures are the same, signature on cheque matches signature on the core-banking, etc.

Output

Based on this, it approves, rejects or flags for human intervention.

Most Salient Features are

- Process Instantly

- Reduce Errors

- Improve Efficiency

- Scale at Will

What does Bank Cheques Automation Segregate?

Segregation is a step in the process that allows separation of all regions of interest as processable or not. Fields in English, both printed and written, will be processed and classified as

- Processable fields. Bank Cheques Automation was able to process the field and promises near 100% accuracy of extracted information. Currently, 85% of all regions of interest can be processed by SnapChek.

- Non-Processable field. Bank Cheques Automation found interferences such as stamp, noise or poor quality of image and crossing lines, that prevented the algorithms from extracting information in an accurate manner. Such fields are sent for manual edit.

- All non-English fields are ignored.

What regions of interest in a Cheque are Extracted?

The following information will be extracted from a cheque by defining the Regions of Interest:

- Amount in words

- Amount in numbers

- Account number of the cheque

- Date of writing the cheque and the validation period of the cheque

- MICR band on the cheque

- IFSC Code

- Signature(s) on the cheque

- Payee Name

Of the data fields above, Amount in Words, Amount in Number, Date and Payee Name could be hand-written or printed. Further those fields could be printed or written in English or another language.

What is Validated?

The validation is done to check whether the information entered in the cheque satisfies the conditions and requirements for clearing the cheque. This is done by various modules.

Date Validation

The date of receiving the cheque must be within the validation period which is within the date on which the cheque was written. A cheque which is received by the bank for processing beyond the validation period will be rejected for clearance.

Amount Validation

The amount written in words is matched with the amount written in numbers.

Account Number Validation

MICR extracted from the cheque is cross-referenced with the bank database to ensure that the account number is extracted correctly.

Signature Validation

The signature entered in the cheque is compared with the drawer’s card signature stored in the bank’s database. A mismatch in the compared signatures or failure to assert the correct number of signatures present will result in rejecting the cheque for clearance.

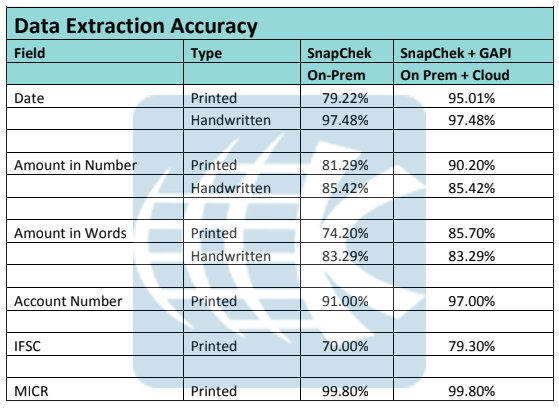

Output Accuracy of Bank Cheques Automation

Currently, Bank Cheques Automation achieves near 100% accuracy of data extraction from truth data of the processable section. As informed earlier, Bank Cheques Automation achieves nearly 85% of the region of interest as processable.

Here is a table of data accuracy for both processable and not processable regions of interest. Usually, printed cheques are about 30% of all cheques drawn. Four hundred cheques, 200 handwritten and 200 printed cheques, all in English, were processed.

SnapChek works as an On-Prem product. Given permission, data is encrypted and transferred over cloud to Google Vision for better performance on data extraction. The above data accuracy table was created from application of SnapChek on a set of standard bank cheques. However, the data accuracy may differ based on a bank’s own context. For example, in our experience, we found several differences in the regions of interest across banks:

- Account number length differed

- The lines under the Amount in Words were not line but micro-letters of the bank name

Manual Override

A manual override can be performed over the extracted information and the final decision regarding the clearance can be performed by an auditor present in person. The auditor has the authority to do the following

- In case of false extracted information he/she should be able to edit the scanned information

- If the scanned cheque is rejected for clearance due to an unknown reason in validating any of the extracted information, he/she has the power to reverse the decision and clear the cheque.

- This inverse case is also possible, he/she can reject the cheque for clearance even when the software has validated the cheque, for example, when the entered amount in words and digits match but is not the same as the extracted information.